Warning: steer clear of extended auto loans

Don't fall victim to "negative equity"

Don't fall victim to "negative equity"

Don’t get conned into buying more car than you can actually afford the next time you’re at your local auto dealership. Troubling findings from the Financial Consumer Agency of Canada show that a growing number of consumers are purchasing bigger vehicles with larger extended auto loans exceeding the standard five years.

This is concerning because monthly payments on longer loans for more expensive vehicles are often roughly the same as those on shorter loans for economy cars. And since most consumers break their auto loans during the fourth year, they’re more likely to refinance debt into their next auto loan—something known as long-term negative equity.

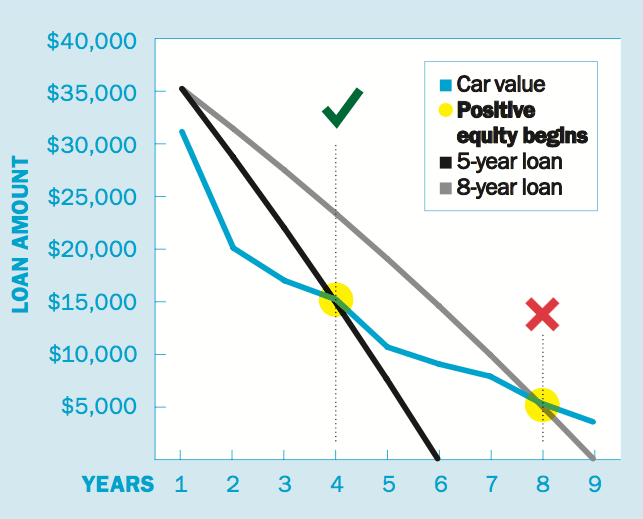

The example below shows how someone who bought a $35,000 car, financed with a 4% interest rate loan over five years, would start accumulating positive equity—in which the car’s value becomes greater than its loan balance—midway in the fourth year. Meanwhile, someone who bought the same vehicle with the same rate over eight years is still $9,000 underwater halfway through year four and won’t start acquiring positive equity until the end of the seventh year.

Read more:

Should I get a long-term loan? »

How to get out of a bad car loan »

Buying your first car »

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Mazda’s beloved two-seater convertible is fast, fun and fabulous to drive. Here’s how to find a good used one.

The hardworking GMC Yukon offers the best value among used SUVs in Canada—especially if it has a Duramax diesel...

I peer deep into the Kia Soul for this review—and I like what I see. Find out why this...

Canadian families adore the Dodge Grand Caravan. Here’s why it offers great value as a second-hand minivan—and what to...

The Ford Escape entered its fourth and current generation in 2020—alongside a compelling hybrid-powered variant. Our review outlines its...

This hardworking pickup is still the bestselling vehicle in North America. Here’s how to choose a great pre-owned F-150...

The Corolla is Toyota’s bestselling vehicle, as it’s easy to see why. Here’s what we love about it, inside...

If you want luxury without a sky-high price tag, consider Lexus’ entry-level sedan. Here’s what to look for when...

Looking for a used large luxury car? Consider a Genesis G90. Here’s why it’s one of Canada’s best pre-owned...

This fun-to-drive, reliable and roomy ride is our pick for the best used family sedan in Canada—find out why.