Tangerine credit card review: Is it the best no-fee card in Canada?

You’ve heard the buzz about this no-fee cash back card, but is it worth the hype? And how does it stack up against the competition?

Advertisement

You’ve heard the buzz about this no-fee cash back card, but is it worth the hype? And how does it stack up against the competition?

With high inflation rates in Canada, you may be looking for creative ways to save money. And while a cash back credit card can be an easy way to put money back in your pocket from spending on essentials like groceries and gas, most cash back cards worth swiping come with a substantial annual fee.

Enter the Tangerine Money Back Mastercard. We like the generous welcome offer, solid earn rate, and a few other perks. So, is the Tangerine Money Back Mastercard the best no-fee cash-back card for Canadians? We break down the online bank’s offerings and see how it stacks up against its competitors.

Annual fee: $0

Welcome offer: Earn an extra 10% cash back during the first two months (up to $100 in cash back). Offer expires January 30, 2026

Card details

| Interest rates | 20.95% on purchases, 22.95% on cash advances and 22.95% on balance transfers |

| Income required | Personal or household income of $12,000 |

| Credit score | 660 or higher |

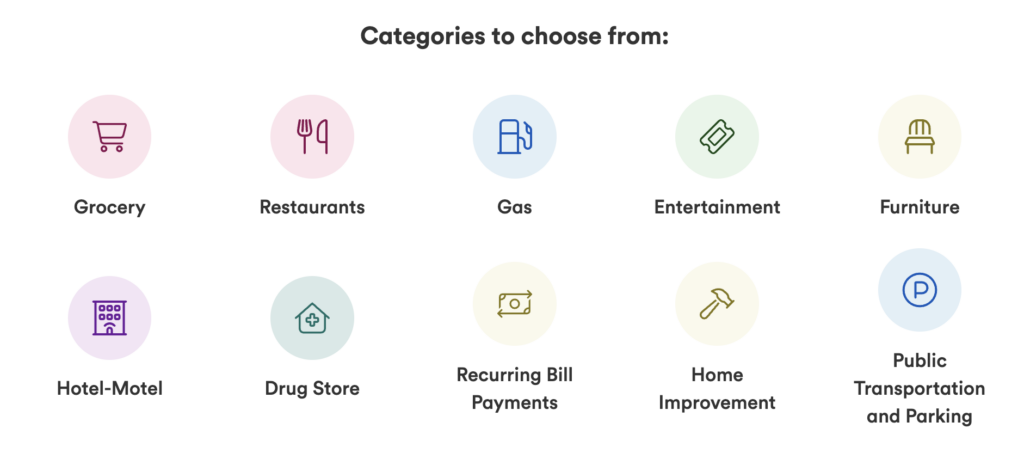

The Tangerine Money-Back Credit Card offers 2% cash back in your choice of two (out of 10) spending categories. If you have your cash-back earnings deposited into a Tangerine savings account, you’ll get to choose a third category in which to earn that boosted 2% earn rate. For context, most other no-fee rewards credit cards either earn fewer rewards per $1 spent or offer fewer bonus categories. And there’s even more…

What really sets the Tangerine Money-Back Mastercard apart from the rest is that it’s the only credit card in Canada that lets you pick your own bonus categories. You can align these with your spending and use this feature to maximize your rewards. (Speaking of inflation, gas and groceries could be savvy categories to earn cash back on.) Other cards may give you a higher earn rate, but it could be in a category you barely use.

Pro Tip: The boosted categories you choose aren’t set in stone. You can switch categories (via the app) whenever you’d like for the first time and every 90 days after that, ensuring you’re earnings match your highest spending categories.

The card’s welcome offer allows you to earn an extra 10% back on up to $1,000 in everyday purchases within the first 2 months. It’s almost like a reverse annual fee. You’re paid you to use the card—if you plan to spend that much in the first two months anyway.

The cash back you earn from your boosted categories is deposited in your account on a monthly basis. And unlike many cash-back cards, there’s no cap on your earnings.

If you need to consolidate debt from another credit card, the Tangerine card offers a low interest rate on balance transfers for six months. Simply complete the balance transfer request within 30 days of opening your account, and then move your debt over to your Tangerine card.

For the following six months, your transferred balance will only accumulate 1.95% interest. Just be sure to pay off that balance within six months because once the promotional rate ends, you’ll pay the regular 19.95% rate on any remaining debt.

If you’ve got an accumulated balance on another credit card, this promotion can help you consolidate your debt and pay it down at a fraction of the interest.

Note: There is a flat balance transfer fee of 1%. For example, if you transfer $1,000 to your Tangerine card, you’ll pay a $10 balance transfer fee.

Aside from being a good everyday credit card option for Canadians, it’s also extremely flexible since you can switch up your boosted categories every 90 days. This is what makes the card so unique.

Let’s say you have a big renovation coming up. If you’ve selected the home improvement category, you’ll get 2% back on those purchases. Booking a trip? Travellers will do well with the hotel-motel option. Those looking to buy new furniture stand to earn back a healthy percentage. (But changes won’t come into effect immediately, so plan ahead.)

With a bit of planning and selecting the right categories for you, you can stow away some extra money with cash rewards.

There’s also another way to maximize your credit card rewards: pair the Tangerine card with a second credit card to get the most cash back possible on every purchase.

For example, say you choose gas, restaurants, and groceries as your three 2% cash back categories on your Tangerine card, but you want to buy a new couch. You can purchase the sofa with another credit card that has a higher cash-back rate than Tangerine’s base 0.5%—such as the SimplyCash Card from American Express card*, which has a cash back rate of 1.25%—and earn maximum rewards.

No-fee credit cards like the Tangerine Money-Back Mastercard don’t tend to offer much in the way of perks. You get basic credit card insurance, like purchase protection and extended warranty, but that’s pretty much it. If you earn a personal annual income of $60,000 or more (or household income of at least $100,000), you could qualify for the higher-tier Tangerine World Mastercard. The Tangerine World Mastercard is virtually identical to the Tangerine Money-Back credit card, offering the same in cash back rewards while also charging no annual fee—but it includes some additional perks.

The amount you can earn with the Tangerine Money-Back card varies depending on your spending habits. To give you some idea of the earning potential, we chose three common bonus categories—groceries, recurring bills, and dining—while assuming a monthly budget of $2,000 is spent as follows:

| Spending category | Earn rate | Monthly spend | Annual reward |

|---|---|---|---|

| Groceries | 2% | $500 | $120 |

| Recurring bills | 2% | $200 | $48 |

| Dining | 2% | $300 | $72 |

| Everything else | 0.5% | $1,000 | $60 |

| Total | $2,000 | $300 |

Based on this scenario, you’d earn $300 in cash back annually, which is a nice bonus since the card carries no annual fee.

Tangerine’s unique rewards structure gives you the ability to choose your own bonus categories, which makes it ideal for pairing with another credit card to maximize your rewards as part of a two-card strategy. We like the Tangerine Money-Back in tandem with the SimplyCash Card from American Express*. The latter also has no annual fee but earns a flat 1.25% on everything you buy. With this strategy, you’d use the Tangerine card for purchases in accelerated categories and the SimplyCash from American Express for everything else in order to collect more cash back.

| Spending category | Credit card and earn rate | Monthly spend | Annual reward |

|---|---|---|---|

| Groceries | Tangerine Money-Back 2% | $500 | $120 |

| Recurring bills | Tangerine Money-Back 2% | $200 | $48 |

| Dining | Tangerine Money-Back 2% | $300 | $72 |

| Everything else | SimplyCash Card from American Express 1.25% | $1,000 | $150 |

| Total | $2,000 | $390 |

By simply using these cards together, you can bump up your annual earnings by $90—all without any annual fees.

The regular cash back rate on the Tangerine card is only 0.5%, which is better than nothing but it’s not going to make headlines. Also, there’s not much on offer by way of extras with this card (for instance, it lacks travel insurance benefits) though the standard purchase protection and extended warranty apply.

Truth be told, there aren’t many products that compare to the Tangerine Money-Back card since no other card lets you pick your own bonus categories. However, these cards deserve consideration, too.

Though less flexible than the Tangerine card, this credit card from Simplii offers a huge 4% back on purchases at restaurants, coffee shops and bars up to $5,000 annually, and 1.5% back on gas, groceries, drug store purchases and pre-authorized payments up to $15,000 per year. Once a cardholder reaches those limits, they earn at the default 0.5%. For those who dine out frequently, this can be an excellent choice.

Annual fee: No annual fee

Welcome offer: Earn 20% cashback for your first 3 months on up to $500 spend on eligible gas, groceries, drugstore purchases and pre-authorized payments.

Card details

| Interest rates | 20.99% on purchases, 22.99% on cash advances, 22.99% on balance transfers |

| Income required | $15,000 per year |

| Credit score | 660 or higher |

SimplyCash Card from American Express offers a competitive cash back rate of 2% on gas and groceries, plus a 1.25% base rate on all other purchases, making it one of the best cash back cards in Canada. American Express adds a boost with $100,000 in travel accident insurance and access to virtual events and special offers with American Express Experiences.

Annual fee: $0

Welcome offer: Earn a bonus 5% cash back on your first $2,000 in purchases during your first three months (up to $100 in bonus cash back).

Card details

| Interest rates | 21.99% on purchases, 21.99% on cash advances, penalty APR on purchases and cash advances (rates are variable) |

| Income required | None specified |

| Credit score | 725 or higher |

We’ve outlined this card’s valuable perks and earnings. These questions will help you determine the best product for your situation. Here are some questions to help you figure that out.

Affiliate (monetized) links can sometimes result in a payment to MoneySense (owned by Ratehub Inc.), which helps our website stay free to our users. If a link has an asterisk (*) or is labelled as “Featured,” it is an affiliate link. If a link is labelled as “Sponsored,” it is a paid placement, which may or may not have an affiliate link. Our editorial content will never be influenced by these links. We are committed to looking at all available products in the market. Where a product ranks in our article, and whether or not it’s included in the first place, is never driven by compensation. For more details, read our MoneySense Monetization policy.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

The Bank of Canada holds its key rate at 2.25%, keeping variable mortgage rates and savings returns steady amid...

Global conflicts affect Canadians’ finances in real time. Learn how rising costs, volatility, and uncertainty can impact your budget...

If you leave Canada and own a rental property, or you are a non-resident and you buy a rental...

Global airlines, including Air Canada and WestJet, are raising fares and fuel surcharges as jet fuel prices soar following...

Rental property investors need to report their annual income and expenses on their tax return. You must also track...

Used car prices remain high in 2026, pushing buyers to put down less and finance more. Here’s how insurance...

Parents can help their kids buy a first home without risking their own finances. Explore smart strategies, from FHSAs...

A PolicyMe study reveals how Canadians choose term life insurance, including coverage amounts, beneficiaries, and generational trends shaping 2026...

A pricing error could work in your favour. Discover how Canada’s Scanner Price Accuracy Code compensates shoppers—and its important...

Sponsored By

RBC

Does anyone know what category I would choose for a cosmetic surgery? I have laser eye surgery coming up and wonder if this would be useful…

Does any credit card give more than 0.5% on Costco shopping ? I would love to get that!

The Costco MasterCard is worth mentioning. 2% on purchases at Costco as well as restaurants and I think gas. 1% on everything else

Correction. The Costco MasterCard gives you 3% back on restaurants. The card itself is free but you do have to have a costco membership.

@Suzi Skinner

Correction: You do get 2% back on Costco gas but only 1% back on store purchases at Costco.

Is this an update of the article…comments go back to Nov 2020, and Costco now has a new MasterCard provider and I’m not sure if cash back offers as the same as with previous provider.

I own a Tangerine MC and I cannot be happier. I set up to pay all my bills automatically with this card, that bring me roughly $20-25 cash back.