How to read your mortgage documents

A snapshot of typical mortgage documents and a few tips on what to watch out for

A snapshot of typical mortgage documents and a few tips on what to watch out for

Thomas Bruner was a well-informed and financially savvy shopper. Thank goodness. Because his bank made errors in his mortgage documents. Big errors.

It was late 2015 and Bruner and his wife, Leslie, were in the process of selling their North York town-home to move into a larger upper beaches family home in the east end of Toronto. (We’ve changed names to protect privacy.) As a number-cruncher, Bruner knew how important it was to shop around for the best mortgage rate and was delighted to secure a five-year fixed rate of 2.49% with his current bank. To get that rate, he’d shopped around and negotiated hard with the bank representative at his local branch. But when the purchase of the home was closer to being finalized, Bruner was transferred to a bank mortgage specialist. That’s when the problems started.

A meticulous man, Bruner read every word of the 30-page mortgage document—some of it in small, fine print, and other sections bogged down with legal jargon. An hour later, Bruner emerged stunned. His bank had made a mistake. A big mistake. A mistake that added $100s to his monthly payments and tens of thousands in interest over the life of the mortgage.

Instead of 2.49%, they’d calculated his mortgage payments based on a rate of 2.99%. The bank had also changed the rate of payments from biweekly to monthly. If he’d signed the mortgage documents without reading the package, he would’ve paid more than $4,075 in extra interest payment,over the five year term*. That’s no small change. (*Assumes a $450,000 mortgage amortized over 25 years, interest calculated based on a five-year term.)

So, Bruner called the bank’s mortgage specialist. Rather than apologize and amend the error, the mortgage rep tried to argue that this was now the going mortgage rate—the best the bank could offer. Bruner was stunned, yet again. “I argued back,” he recalls, “explaining that we had locked in our rate during the pre-approval process. We were only 40-or-so days into the 90-day rate-hold guarantee.”

Bruner isn’t the only one to notice problems. According to the Ombudsman for Banking Services and Investments (OBSI), errors made by the banks rank No. 4 in the top 10 reasons for customer complaints. However, when asked for specific statistics on the precise number of complaints lodged, and how many of these complaints directly relate to errors in mortgage documents, an OBSI spokesperson replied that they don’t release this information. Instead, the OBSI offers very pretty spiderweb and sunburst visual representations of customer complaints.

This lack of transparency prompts the question: How many other people have been screwed by a professional working in the real estate market? (Cue the wrath of every bank, mortgage broker, home inspector, insurance agent, realtor and renovator involved in this industry.)

Still, how many of us signed a document only to realize, after the fact, that there was an extra charge? Or found an error that’s in the lender’s favour? While reading every page of every legal document we sign is the smart, prudent thing to do, truth be told very few of us understand all of what’s written in an insurance contract, mortgage document or even a purchase and sale agreement.

To help, here’s a snapshot of typical mortgage documents and a few tips on what to watch out for—keep in mind every lender have their own versions of this document, so this is meant to be illustrative only.

To help you process the information, consider the following.

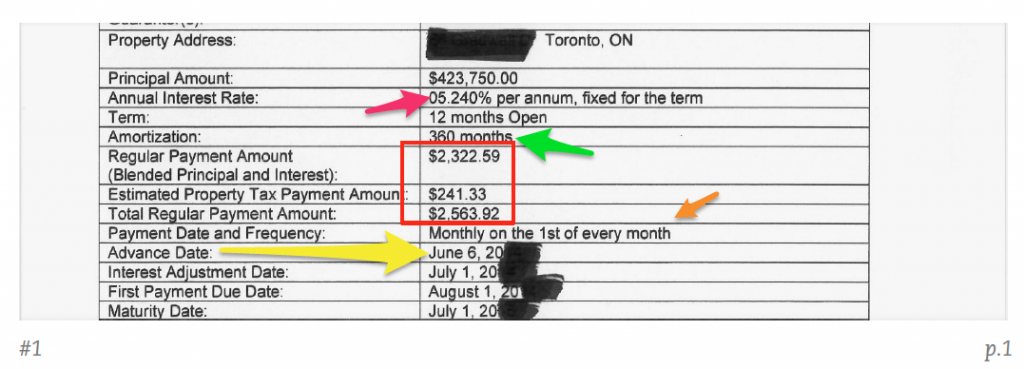

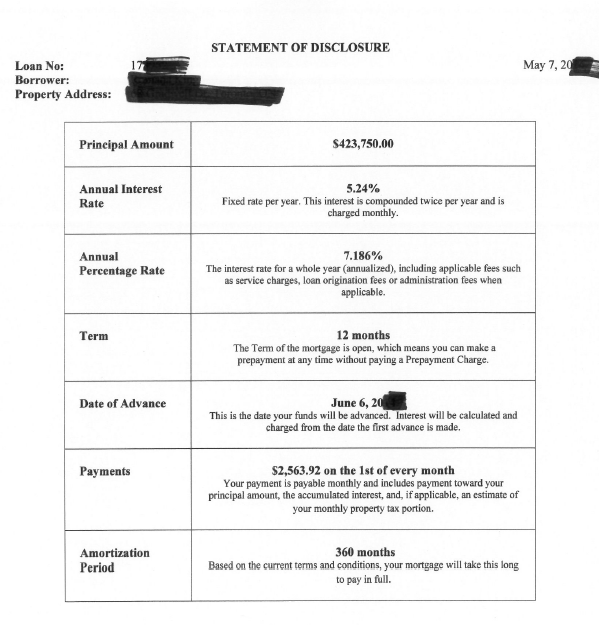

The pink arrow points to the mortgage interest rate that you will be charged during the duration of the loan term. Check this. Even a 10 basis point change in the rate can add up over the long haul.

The green arrow points to the length of your amortization, expressed by the number of months. Check this. Some of the biggest mortgage document errors are in how long a loan is amortized for; while a cheaper monthly rate can seem appealing, this sort of error can tack on tens of thousands of extra interest costs over time. Above this amortization rate, is your term length—how long you’re committed to pay this lender, based on the rates and terms you’ve both agreed upon. The line should also state whether you’ve agreed to a fixed, variable or open mortgage. . The type of mortgage you agree to can have serious implications on the penalties you’re charged should you opt to make an extra payment, or break your mortgage agreement. For simplicity sake, a one year mortgage is expressed as 12 months, while a five-year mortgage term is expressed as 60 months and a 25 years amortization is expressed as 300 months.

Read more: At mortgage renewal what’s best, a fixed or variable rate »

The three numbers in the red box reflect the monthly mortgage rate you will pay (a mixture of principal plus interest), the monthly property tax you will pay to your bank (who will then make a payment on your behalf) and the total amount you will pay based on the addition of these two amounts. If you want to double-check your lender’s math, try Karl’s Mortgage calculator.

The orange arrow is how frequently you will make payments to your lender. Check this. Not only does payment frequency help reduce the overall interest you end up paying, but to make changes after you’ve signed your document can cost you an out-of-pocket fee.

The yellow arrow is the day you first get your money and the day the interest clock starts ticking. Pay attention to this. Some lenders will charge you a larger amount for the first payment of your mortgage to cover the interest that has accrued from the Advance Date to the day you make a payment against the outstanding loan. Some lenders don’t increase the first payment, but allocate a larger portion of this payment to pay off the outstanding interest. Either way, you want to be clear about what’s being charged, and when.

Under the property taxes clause you will notice that the monthly sum added to your mortgage payment is an “estimate” based on the lender’s assessment of your annual property taxes. If you don’t want to pay your property tax monthly or you want to amend how much you pay you’ll need to negotiate this with your lender.

In recent years, we’ve heard a lot about mortgage penalty fees. You pay these penalties to your lender whenever you break the negotiated terms of your loan contract. If you have an open mortgage, there should be no penalties for pre-payments or to pay-off the entire loan before the end of the negotiated term. If you have a variable-rate mortgage, you will be charged a penalty that’s equivalent to three months of mortgage payments, plus administrative fees. If you have a fixed-rate mortgage, you will be charged a fee that’s calculated using the Interest Rate Differential calculation. This calculation is different for every lender, but it can add up, quickly.

Read more: Six steps to lower your IRD mortgage penalty »

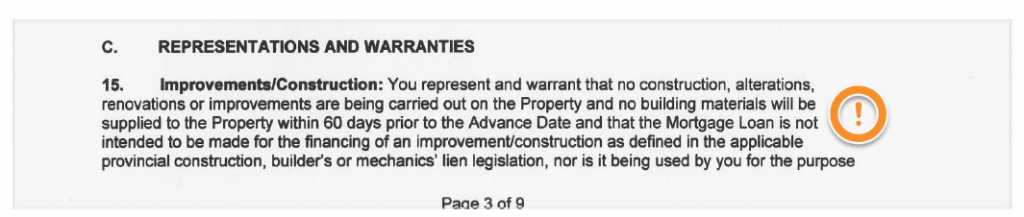

Many homebuyers are shocked to learn that they can void their home insurance policy if they undertake home modifications or renovations without first notifying the insurance company and, typically, paying an additional premium. But did you know you can also void your mortgage loan contract—and prompt a lender to recall and cancel the loan—if you obtain a mortgage and don’t disclose intended construction, alterations or renovations to the home? Read your mortgage contract carefully to see exactly what must be disclosed.

When reading your mortgage contract the lender will typically list the type of documents you are required to submit in order to verify the information you have provided. This will include pay-stubs, Notice of Assessments for your income tax, as well as additional loan or income verification. But don’t be surprised if your lender follows up with requests for additional documentation. Typically, they cover this off with a broad statement that notifies you that any information they request must be provided. A sample of this type of statement is above, in the red square highlight.

Read more: Documents you need to get the best mortgage rate »

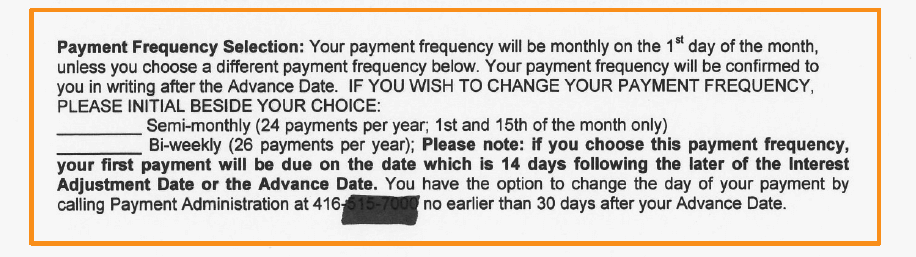

Do you have a plan to pay off your mortgage quickly? Part of that plan may include how often you pay your mortgage—the more frequent the payments, the more you pay and that means paying off the principal faster, which reduces the overall interest you pay for the loan. Every mortgage document will have an area where you can choose the frequency of payments. Be sure to check off your selection, as making change after the document is signed will cost you, as you can see below (in the red circle).

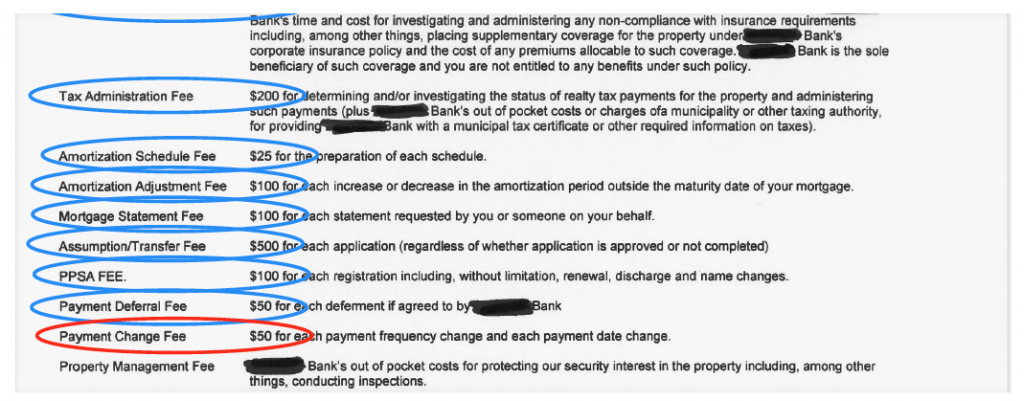

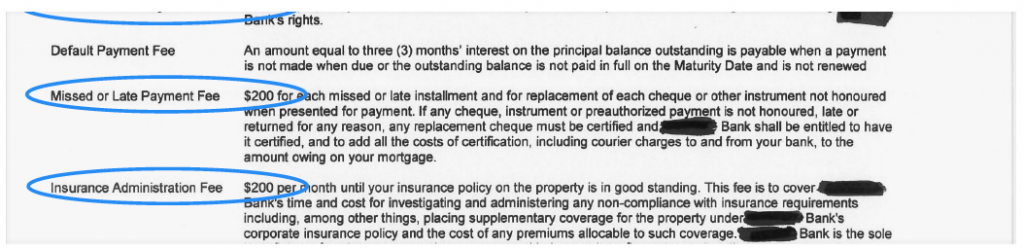

Administrative fees to open and close a mortgage loan can add up. Ask for an amortization schedule—to verify how much of each payment is going towards the principal and how much is interest—and you’ll need to pay your lender. Want a mortgage statement? Fork out more money. Need to renew, you may be slapped with an additional fee. But the one that can be annoying, even if it is relatively minor, is the “Payment Change Fee” (highlighted in red). If there’s an error in your payment frequency in mortgage document you signed and you phone to make a correction, this lender will slap you with a $50 fee. Not your error, but it is your penalty. To avoid paying unnecessary fees, make sure to check your mortgage documents for inaccuracies.

Did you buy a home but forget to shop for a home insurance policy? If your mortgage advance date arrives and you still haven’t been able to submit valid home insurance to your lender, expect a fee. For example, this lender charges $200 per month until you can provide evidence of a valid insurance policy for the home.

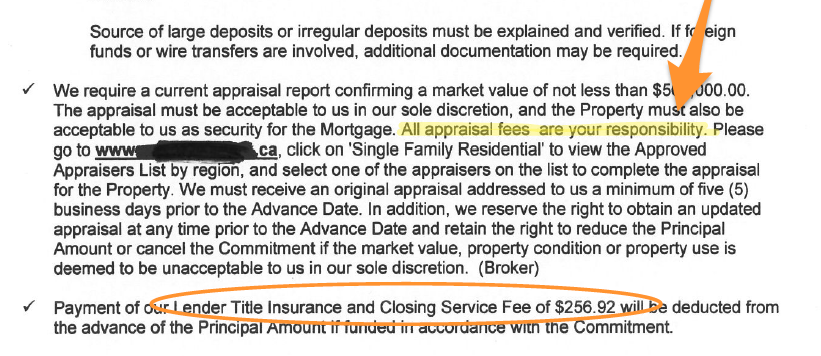

Did your lender ask for an appraisal on the home you want to buy? Don’t be surprised if you have to pay for that report (see highlights above). Plus, some lenders who require title insurance will deduct it from the total amount loaned to you; it’s only a few hundred dollars, but it can leave you scratching your head as to why you didn’t get your full mortgage-loan amount.

Read more: Pay $500 to find out your home’s fair market value »

Have questions or concerns about your mortgage documents? In your contract you should see a clause that clearly states how to get in touch with your lender or how to lodge a complaint. If this doesn’t work, and you’ve worked with a mortgage broker, contact the broker directly. They should work on your behalf to sort out any discrepancies with the lender. Finally, if your independent broker isn’t helpful or if you went through a bank to get a loan and you’re not getting anywhere, consider contacting the bank’s ombudsman. This is an independent role within a financial institution that’s tasked with addressing consumer complaints. If this fails, consider lodging a complaint with OBSI. But be warned: It can take up to nine months just to get an answer on a complaint, sometimes longer.

Finally, almost all lenders now provide a synopsis of all fees and terms in that back of your loan document. This doesn’t mean you should skip over the body of the document, but this summary is a great spot to start verifying if key terms, such as the mortgage rate and the length of amortization, is accurate. If not, mark it, and go back to your lender. Don’t be afraid to fight for what you agreed to. Bruner wasn’t.

Despite the reluctance by his bank’s mortgage specialist, Bruner eventually got the rate he was initially promised. One key component to his negotiations were the emails he’d kept. The correspondence was evidence of what Bruner was promised and made it hard for the bank to rescind the initial offer.

Affiliate (monetized) links can sometimes result in a payment to MoneySense (owned by Ratehub Inc.), which helps our website stay free to our users. If a link has an asterisk (*) or is labelled as “Featured,” it is an affiliate link. If a link is labelled as “Sponsored,” it is a paid placement, which may or may not have an affiliate link. Our editorial content will never be influenced by these links. We are committed to looking at all available products in the market. Where a product ranks in our article, and whether or not it’s included in the first place, is never driven by compensation. For more details, read our MoneySense Monetization policy.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Understanding industry jargon can make you a better real estate investor.

Learn how the federal government’s 2024 budget can affect you and your money.

The federal government is also raising the amount Canadians can pull from their RRSP to purchase a home through...

Created By

Ratehub

Canada may be likely to avoid a recession, but we won’t start recovering until the second half of 2024,...

Do Canadians have to file a trust tax return this year? What is a bare trust? What are the...

A new CMHC report says construction of new homes in Canada’s six largest cities remained near all-time high levels...

Financial experts debunk old money myths and offer advice that many Canadians might find more helpful today.

Presented By

National Bank of Canada

Hi I live in Ontario Canada, my lender wrote up my mortage papers to reflect that there are 2 registered owners but there is only 1. This year they paid me 75,00 to have a lawyer put me on title. But what they did before and now is a horror story. Hid a mortage payment , have a in branch payment receipt stating PAID. Sent property management com. to my home when I was at work,do a APPRAISAL, criminal trespass. Branch manager called me out infront of 30 customers employees they had been paying my land taxes for 5 years, I was incompetent and irresponsible. So not true had to get my local mayor to try to help such stupidity. Coned me to sighn a statement of settlement contract ILLEGAL. Did not sighn, just a taste of my hell, I even reached out to prime minister Trudeau. Thanks ReneeJaremek

Hello, one typo 8n my original article TD paid 7,500 to a lawyer I had to hire to put me on title.

This new year they dropped me like a bad habit, billed me thousands of dollars for legal fees.

When my realastate lawyer asked why they were billing me thousands in legal fees TD refused to release the mortage, unless I sighned a waiver that I was not going to sue them. I walk with Jesus, so the devil TD will not push me around. What they did is like holding a gun to my head.

TD has breached their fiduciary responsibilities and caused me severe neglect. I’ve also been presented with a statement of settlement contract, that document is illegal. Alot more I have had to continue to endure, because TD will not admitt when they screwup. ReneeJaremek

Looking for info